The Hidden Cost of Debt: How Financial Stress is Crippling Millions

Debt is more than just a financial burden—it’s a source of immense stress and anxiety for millions. From credit cards to student loans, the weight of unpaid bills can feel overwhelming, as seen in viral TikTok stories of couples drowning in six-figure debt. But what if there was a smarter way to manage debt without losing sleep? This article explores the emotional toll of high debt and introduces a hypothetical SaaS solution designed to alleviate financial stress.

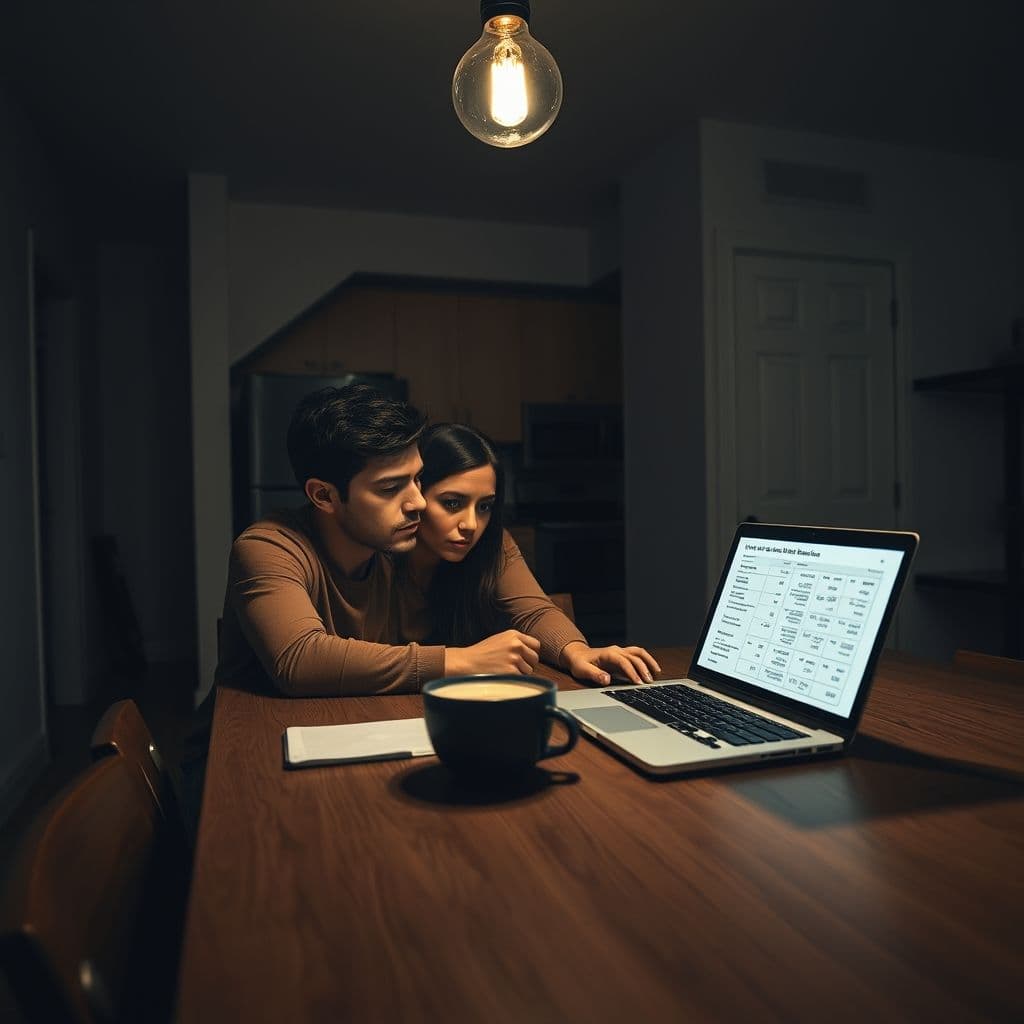

The Problem: Debt and Its Emotional Toll

The comments on viral debt-related TikToks reveal a common theme: stress. Users with as little as $1,500 in debt express sleepless nights, while others with six-figure balances feel trapped. The psychological impact is undeniable—debt doesn’t just drain bank accounts; it erodes mental health. Many admit to feeling judged when seeking help, compounding their anxiety. The problem isn’t just the numbers—it’s the lack of accessible, non-judgmental tools to manage debt effectively.

A Hypothetical SaaS Solution: DebtEase

Imagine a SaaS platform called DebtEase, designed to tackle debt holistically. Unlike traditional budgeting apps, DebtEase would combine financial tracking with mental health support. Key features could include automated debt payoff plans tailored to income, real-time alerts for due payments, and even guided mindfulness exercises to reduce stress. The platform would use AI to analyze spending habits and suggest micro-adjustments, like skipping a daily latte to save $100/month.

DebtEase could also integrate with credit counselors and therapists, offering users a seamless way to access professional help. Gamification elements, like progress bars for debt milestones, might motivate users to stay on track. The goal? To turn the isolating experience of debt into a structured, supportive journey.

Potential Use Cases

DebtEase could serve diverse users: recent graduates drowning in student loans, couples overspending on credit cards, or even small business owners juggling cash flow. For example, a user with $50,000 in student loans might use the app to automate extra payments whenever they get a bonus. Another user could leverage the mental health resources to cope with the shame of debt while rebuilding their credit.

Conclusion

Debt doesn’t have to be a life sentence of stress. While tools like DebtEase are still hypothetical, the demand for compassionate, tech-driven debt solutions is real. By addressing both the financial and emotional sides of debt, such a platform could revolutionize how we approach money management. Until then, the first step is acknowledging the problem—and seeking support, one payment at a time.

Frequently Asked Questions

- How would DebtEase differ from existing budgeting apps?

- Unlike basic budgeting apps, DebtEase would focus specifically on debt payoff, integrating mental health support and personalized AI recommendations to reduce stress and accelerate financial freedom.

- Is this SaaS idea feasible to develop?

- Yes, but it would require collaboration between financial experts, therapists, and developers. Key challenges include ensuring data security and creating an AI that adapts to diverse financial behaviors.

- What’s the first step to managing debt stress?

- Start by listing all debts and interest rates. Even without a tool like DebtEase, awareness is the foundation of any payoff strategy.